Commercial real estate will both prosper and struggle going into 2024. At least that’s how the respondents to Seyfarth Shaw LLP’s ninth annual Real Estate Market Sentiment Survey portrayed the industry.

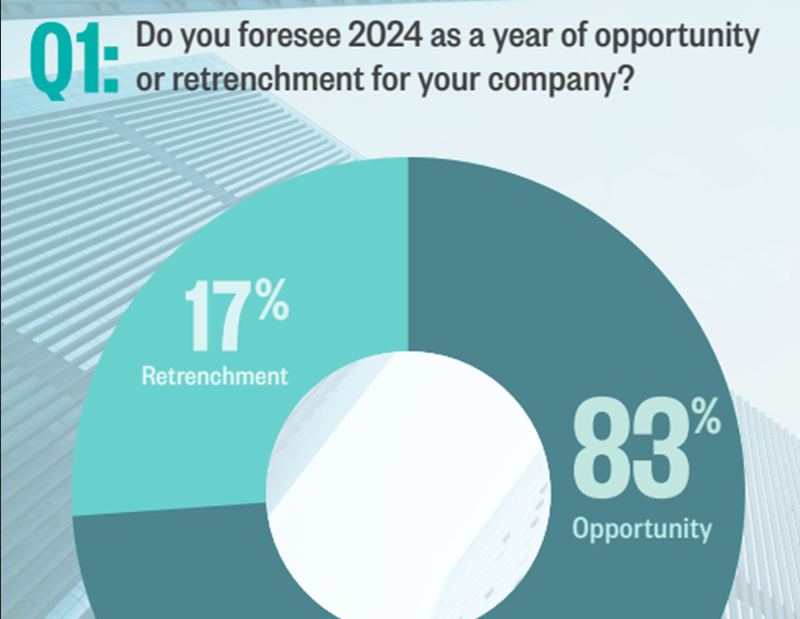

For the survey’s 120 respondents consisting of executives from around the industry, 83 percent answered that they predict that 2024 will be a year of opportunity for their companies, while only 17 percent anticipate a retrenchment. This is a sharp uptick from the 69 and 31 percent that had the same respective sentiments in last year’s survey.

Interest rates, the root of most difficulties

The positivity’s primary cause? Several likely interest rate cuts that 94 percent of respondents see taking place this year. Presently, the Federal funds rate’s target range sits at 5.25 to 5.5 percent, its highest since the Global Financial Crisis.

Still, there were ample divisions about by how many basis points rates will come down. Of the total, 51 percent of those polled anticipate a net decrease of 26 to 50 basis points, while a further 23 percent predict a slash of 50 basis points or more. In addition, 20 percent anticipate no change to rates to a top end of 25-basis-point contraction.

READ ALSO: Why High Interest Rates Present Opportunity for Some

These sentiments come as no surprise, given how respondents ranked their greatest challenges this time around. Interest rates, and the numerous aspects of both commercial real estate operations and the larger economy they impact, ranked first, with 70 percent of those surveyed flagging them as their top challenge. Coming in second was the scarcity of debt financing, identified by 45 percent of executives as their most prominent hurdle. Construction costs took home the bronze, with 37 respondents listing it among their chief hurdles.

But what will happen once interest rates are cut, and how much of a decrease will it take to put transaction volumes on an upswing? For a total of 71 percent of respondents, it will take a baseline of more than a 50-basis-point net decrease in rates for transactions to trend positively, with 49 percent bracketing off a reduction of 51 to 100 basis points, while an additional 21 percent believe that the funds rate needs to decrease by a net 100 basis points.

Deals getting done

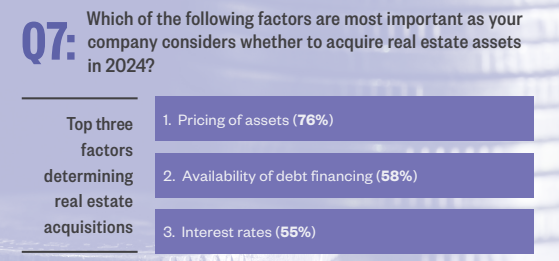

Of course, the magnitude of the rate cuts that determine whether a given acquisition or development closes bleeds into a myriad other factors. For the executives polled by the survey, the top three most important circumstances towards acquiring new assets are their pricing, the availability of debt to finance them and the interest rates themselves.

Here, 76 percent of executives put asset pricing as their most important factor, while debt availability and interest rates were a distant second and third, with a respective 58 and 55 percent of respondents ranking them at the top.

As for raising the capital to fund the deals themselves, equity investments are going strong. Institutional investors and private equity, largely immune to the effects of high interest rates, combined to form 70 percent of respondents’ top sources, outranking self-funding, foreign investors and unidentified contributors.

Tackling the trends

The survey also highlighted some more circumstantial investment trends from around the industry, in particular, interest in distressed assets and conversions of office properties to residential and mixed-use.

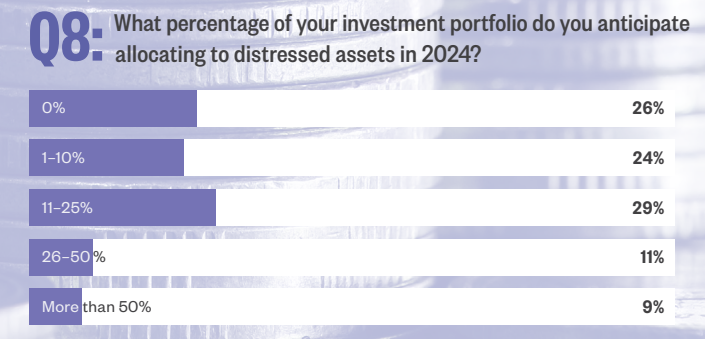

For investment in distressed assets, a total of 74 percent of respondents expressed the intention to allocate between 1 percent and half of their portfolios to distressed properties. Given the $929 billion in commercial mortgages that the Mortgage Bankers Association shows will come due, it will likely be difficult for investors to ignore distressed properties entirely.

Of those respondents, 29 percent intend to invest between 11 and 25 percent, 11 percent stand between 26 and 50 percent, while 9 percent plan on allocating more than half of their portfolio to distressed assets. The second highest contingent, 26 percent, do not intend to pay distressed assets any mind at all.

On the conversion front, the projects appear to be on executives’ back burner for now, given the latent difficulties in financing, particularly for intensive construction. Nearly two thirds of respondents—61 percent—stated that they are not likely to invest in conversion projects this year, while 29 percent declared they are somewhat likely to capitalize such endeavors. A combined, even split of 10 percent answered that are either somewhat or very likely to engage in them.