Richard Barkham, Global Chief Economist & Head of Global and Americas Research, CBRE. Image courtesy of CBRE

CBRE expects an economic slowdown in the U.S. next year that will impact commercial real estate with bank lending remaining tight throughout 2024, investment volume decreasing 5 percent, cap rates expanding and property values declining.

But the U.S. may be able to avoid a recession and interest rates should be reduced later in the year as activity picks up in the second half of 2024, according to the firm’s 2024 U.S. real estate outlook.

Property types with relatively strong fundamentals, including demand, vacancy and rent growth, like industrial, retail, multifamily and data centers will be most favored by investors in 2024, according to CBRE.

Richard Barkham, CBRE global chief economist & global head of research, said in prepared remarks there is still some more pain ahead for the commercial real estate industry in 2024, including overall investment volumes remaining down for the year. But he expects an upturn by the second half and overall leasing activity to pick up as well. He notes stabilization and the early stages of recovery are also not far off.

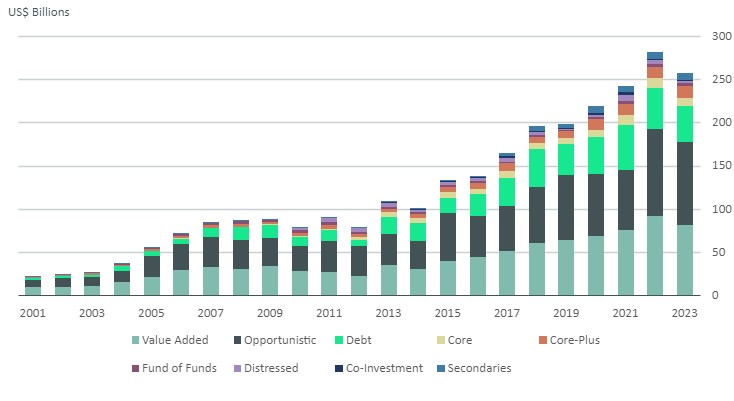

North America dry powder by strategy. Chart courtesy of CBRE

With inflation easing, the Federal Reserve is expected to begin reducing short-term interest rates in 2024, possibly to around 4.25 percent by the end of the year and to 3.5 percent in 2025.

There should be buying opportunities in the first half of 2024, especially for all-cash buyers like sovereign wealth funds, pension funds and endowments. CBRE expects the lowest pricing for assets will occur in the first two quarters.

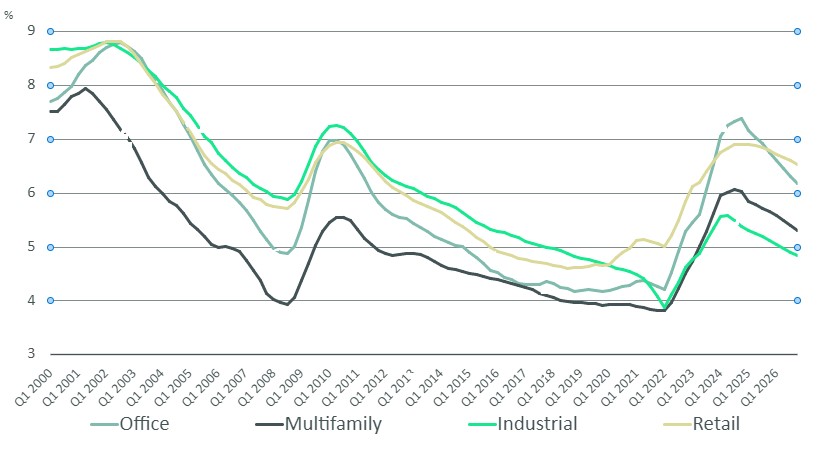

The report notes increasing cap rates, which have risen by about 150 basis points between early 2022 and late 2023 depending on the market and asset type, imply a 20 percent decline in values for most property types. For office, the increase was higher, rising by at least 200 basis points.

“We think cap rates will expand by another 25 to 50 basis points in 2024, with a corresponding 5 percent to 15 percent decrease in values,” the report states.

CBRE expects real estate values for most property types will likely not stabilize before mid-2024.

Historical & forecast cap rates. Chart courtesy of CBRE

Office vacancies to peak

The outlook expects another tough year ahead for the office market with office vacancy peaking at nearly 20 percent in 2024, up from 18.4 in the third quarter of 2023 and 12.1 percent at the end of 2019.

CBRE notes a slowing economy in the first part of 2024 and increasing acceptance of hybrid working arrangements will continue to limit office demand next year. The 2023 U.S. Office Occupier Sentiment Survey found more than half of the respondents planned to further reduce their office space in 2024.

Companies looking to lease less than 20,000 square feet will account for most of the leasing activity, according to CBRE. Leasing activity should rise by 5 percent in 2024, however that is still 20 to 25 percent lower than pre-pandemic levels.

READ ALSO: How Incentives Boost Office Conversions

Meanwhile, the flight-to-quality trend should continue with occupiers seeking space in newer, prime office properties with the best amenities. But office construction levels will be at their lowest levels since 2024, which could result in a shortage of that sought-after Class A space later in the year. CBRE forecasts that average prime office asking rent will increase by as much as 3 percent.

On the investment side, the higher-for-longer outlook for interest rates will cause some owners of Class B and C office assets to sell due to further erosion in values. Many of those older buildings that lack modern amenities will continue to struggle to attract tenants, so a higher percentage of older office assets are likely to be converted to other uses. While office conversions can be challenging, the report notes the federal government is providing grants, low-interest loans and tax incentives and local governments are also offering incentives.

Not all office markets are suffering, and the outlook shines a light on several active cities in the U.S. In Nashville, Tenn., where absorption and rents are up, demand for new office space is expected to remain strong. Miami is seeing one of the highest rent increases in the country and the vacancy rate is dropping as new-to-the market tenants are keeping the market healthy. Las Vegas has seen an uptick in leasing activity and strong preleasing at speculative projects, putting the market in a strong position heading into 2024.

Industrial sector slowdown

The industrial sector should see net absorption similar to 2023 levels and rent growth moderating to 8 percent. Construction deliveries are tapering off and expected to continue to slow down due to economic uncertainty, tight lending conditions and oversupply in some markets.

READ ALSO: Property Management Success: How AI Boosts Industrial

Vacancy is expected to hit 5 percent by mid-2024, up from 4.2 percent in the third quarter of 2023 but decrease later in the year due to the decline in new construction. Looking ahead, CBRE is forecasting a 7.5 percent increase in U.S. industrial production over the next five years as more occupiers improve their supply chains by adding more import locations and onshoring or nearshoring of manufacturing operations. Markets to watch include Austin and San Antonio in Texas; Nashville; Salt Lake City and Central Florida.

Retail’s declining availability

The retail sector is also facing a lack of new construction. That will contribute to retail availability rates dropping by 20 basis points next year to 4.6 percent. Asking rent growth is expected to drop below 2 percent for most of 2024 but go above 2 percent by the fourth quarter.

READ ALSO: Mixed Shopping Cart for Retail

Open-air suburban retail centers will see demand grow faster than other retail formats and neighborhood, community and strip centers will have stable occupancy throughout the year. Look for traditional mall-based retailers to seek other new formats outside the malls for expansion. Texas markets are expected to see more luxury brands. Other markets to watch include Orlando, Fla.; Charlotte, N.C.; Denver; San Francisco and Orange County, Calif.

AI to fuel increased data center demand

The data center market is seeing growth, often driven by advances in cloud-based solutions, artificial intelligence and other new applications and technologies. CBRE notes demand will continue to be higher than supply and construction in major markets will exceed 3,000 MW in 2024, up from the company’s 2023 estimate of 2.500 MW. Markets to watch include Austin; San Antonio and Omaha, Neb.